Chapter 49 — Exchange Rates

Cambridge International AS & A Level Economics (9708) · Unit 11.2 · 4th edition coursebook

Learning objectives

- Identify the three main ways exchange rates are measured: nominal, real and trade-weighted exchange rates.

- Explain the difference between nominal and real exchange rates.

- Explain trade-weighted exchange rates.

- Analyse how exchange rates are determined under fixed and managed systems.

- Explain the difference between revaluation and devaluation of a fixed exchange rate.

- Analyse the causes of changes in the exchange rate under different exchange rate systems.

- Evaluate the effects of changing exchange rates on the external economy using the Marshall-Lerner condition and J-curve analysis.

Key terms

- real exchange rate

- A currency's value in terms of its real purchasing power.

- trade-weighted exchange rate

- The price of one currency against a basket of currencies.

- fixed exchange rate

- An exchange rate set by the government and maintained by the central bank.

- devaluation

- A decision by the government to lower the international price of the country's currency.

- revaluation

- A decision by the government to raise the international price of the country's currency.

- managed system

- Where the exchange rate is influenced by state intervention.

- Marshall-Lerner condition

- The requirement that for a fall in the exchange rate to be successful in reducing a current account deficit, the sum of the price elasticities of demand for exports and imports must be greater than 1.

- J curve effect

- A fall in the exchange rate causing an increase in a current account deficit before it reduces it due to the time it takes for demand to respond.

49.1Measurement of exchange rates

The price of a currency can be measured in three main ways: against another single currency, against what it can buy in another country, and against a basket of currencies.

Nominal and real exchange rates

The nominal foreign exchange rate is simply the price of one currency in terms of another - the number on the foreign exchange board.

A real exchange rate goes further by taking inflation into account. A fall in the nominal exchange rate is expected to make exports more price-competitive, but if the country has high inflation, export prices in domestic currency may still be rising. The real exchange rate compares the relative price of two countries' products and is calculated as:

Real exchange rate = (nominal exchange rate × domestic price index) / foreign price index

The real exchange rate can rise either because the nominal rate appreciates or because the country's inflation rate rises relative to its trading partners. Either way, the country's products become more expensive relative to those produced abroad: more imports can be bought for a given quantity of exports, and over time the country tends to import more and export less. Because the real exchange rate captures international price competitiveness, it has a stronger influence on the current account balance than the nominal rate.

Trade-weighted exchange rate

Most countries trade with many partners, and a currency can rise against some currencies while falling against others. To gauge the overall change in a currency's value, economists use a trade-weighted exchange rate - an index of the currency against a basket of others, with each currency weighted by the size of the country's trade with that partner. A partner that accounts for three times as much trade as another carries three times the weight in the index.

Devaluation is most attractive when inflation is low (so the price competitiveness gain is not eroded) and unemployment is high (so a boost to exports and the trade balance is needed).

Apply the trade weights: country Y has 60% weight and X's currency falls 20% against Y, contributing 0.6 × (−20) = −12. Country Z has 40% weight and X's currency rises 10% against Z, contributing 0.4 × (+10) = +4. The net change is −8. Starting at 100, the new index is 100 − 8 = 92.

49.2Determination of exchange rates

Exchange rates can be set by a government, left to the market forces of demand and supply, or determined by a combination of the two. Most governments and their central banks today allow market forces to play a large role in determining the price of their currency, but reserve the right to intervene when fluctuations in value become too large.

A fixed exchange rate system

In a fixed exchange rate system, the price of the currency is determined by the government and the central bank is charged with maintaining that price. The central bank has two broad tools. The first is direct intervention in the foreign exchange market: the bank buys its own currency when there is downward pressure on the rate and sells its own currency when there is upward pressure. The second is indirect intervention through the rate of interest, which the central bank changes to influence the underlying demand for and supply of the currency.

The interest-rate channel works through hot money flows. Suppose supply of the currency is rising on the foreign exchange market - perhaps because residents are importing more - and the rate is being pushed below its target. The central bank can buy its own currency directly, but it can also raise the rate of interest. The higher interest rate attracts hot money from abroad: foreign savers buy the currency to place it in accounts in the country's financial institutions. The extra demand for the currency offsets the original increase in supply and supports the fixed rate.

Diagrammatically, the target rate is shown as a horizontal line on the foreign-exchange diagram, with quantity of the currency on the horizontal axis and its price on the vertical axis. Starting from equilibrium at the target rate, suppose supply shifts rightwards from S to S1. Without intervention, the price would fall. To prevent this, the central bank buys the currency, which shifts the demand curve rightwards from D to D1 by enough to restore equilibrium at the original fixed price. The reverse case applies if demand falls or supply contracts: the bank then sells from reserves.

A fixed rate is easier to defend if it is set close to the long-run equilibrium value of the currency, because the central bank then only has to offset short-run - and possibly relatively small - fluctuations. If, however, the rate is set well above the market-clearing level (an overvalued rate), the bank risks running out of the foreign reserves it needs to keep buying its own currency, and the fixed rate may eventually have to give way.

The main drawback of a fixed rate is the need to hold reserves. The foreign exchange or gold held for this purpose involves an opportunity cost, because it could otherwise be used for investment, public spending, or other purposes. A government may also be forced to sacrifice other policy objectives to defend the rate. For example, a central bank may raise the rate of interest to support the currency, but a higher interest rate can reduce aggregate demand and raise unemployment - a real cost to the wider economy.

Market pressures may also mean that the rate at which the currency is fixed has to be changed over time. A reduction in the value of a fixed exchange rate to a lower level is known as a devaluation, while a revaluation occurs when the government raises the exchange rate to a new, higher fixed rate.

Set against these drawbacks, a fixed exchange rate offers two main advantages: certainty and discipline. Certainty about the future value of the currency encourages international trade and investment, because a foreign firm is more willing to set up a branch in the country if it knows how much any revenue it earns will be worth in its own currency. Discipline is imposed on the government to keep inflation low: if domestic prices rise faster than those of trading partners, international competitiveness deteriorates and downward pressure on the fixed rate becomes increasingly hard to resist.

A managed system

A managed system combines features of a floating and a fixed exchange rate (see Figure 49.5). The government allows the rate to be determined by market forces within a given band set around a central value, with an upper limit that the rate must not exceed and a lower limit below which it must not fall. As long as the exchange rate stays inside the band, the central bank takes no action and the rate is free to move with market forces.

If, however, market pressure threatens to push the rate outside the band, the central bank intervenes. Suppose demand for the currency rises sharply and would push the price above the upper band: the central bank sells its own currency, increasing supply and pulling the rate back into the band. If, conversely, demand falls or supply rises so that the rate threatens to drop below the lower band, the central bank buys the currency with foreign reserves. Interest-rate changes can also be used to nudge demand and supply in the desired direction.

A managed system therefore preserves much of the flexibility of a floating rate - the rate can drift with underlying market conditions inside the band - while limiting the volatility that can disrupt trade and investment. Like a fixed rate, however, it still requires reserves and may force the central bank to sacrifice other policy objectives at moments when defending the band is most needed.

Key concept link - Equilibrium and disequilibrium

A fixed exchange rate is easier to maintain if it is set close to its long-run equilibrium price.

49.3Revaluation and devaluation of a fixed exchange rate

A revaluation is a government decision to raise the fixed exchange rate to a new, higher level. If market pressure pulls the currency back down towards the old rate, the central bank defends the higher rate by buying the currency with reserves and, if necessary, raising the interest rate.

A devaluation is a government decision to lower the fixed exchange rate to a new, lower level. If markets push the currency above the new lower target, the central bank sells its own currency to increase supply, holding the price down. It may also reduce the interest rate to make the currency less attractive and increase its supply.

Revaluations and devaluations are made for two broad reasons. The first is that the existing rate is unsustainable - it produces persistent shortages or surpluses of the currency in the foreign exchange market. The second is that revaluation or devaluation is being used deliberately as a policy tool, for example to alter the trade balance or to ease inflationary pressure.

Key concept link - The role of government and issues of equality and equity

A devaluation is likely to benefit firms that export but may harm firms that import raw materials and capital goods and consumers who may now have to pay higher prices.

49.4Changes in the exchange rate under different exchange rate systems

Under a floating system, the exchange rate moves whenever the demand for or supply of the currency changes. Demand rises with greater foreign demand for the country's goods and services, with inflows of direct and portfolio investment, and with speculation that the currency will appreciate. Supply falls when the country buys fewer imports, invests less abroad, and when speculators expect the currency to rise.

Changes under a fixed system

A fixed exchange rate does not move from day to day. When it changes, it is by a deliberate government decision. A government will devalue if it judges the current rate cannot be maintained - for example, when market forces are pushing the rate down and the central bank risks running out of reserves defending the rate, and the government is unwilling to raise interest rates to attract hot money because higher rates would cut economic activity. A government may also devalue as an active policy: a lower currency improves the international competitiveness of exports, can reduce a current account deficit, and can support growth and employment.

A revaluation can be used when there is persistent upward pressure on the currency. The government may not want the central bank to sell large quantities of its currency to hold the rate down, because that adds to the money supply. A revaluation can also help reduce inflationary pressure: a higher exchange rate cuts the price of imports and forces domestic industries to compete on quality and efficiency.

A useful rule is that an exchange rate change alters export prices in foreign currency but alters import prices in domestic currency.

A managed float lets the currency move freely most of the time, but the central bank steps in to keep it within a narrow band or to nudge the band over time. That mix of market determination plus official intervention is precisely a managed float — not a fully fixed rate, a free float, or a trade-weighted measure.

49.5The effects of changing exchange rates on the external economy

How a change in the exchange rate affects the current account balance depends on the price elasticities of demand for exports and imports.

The Marshall-Lerner condition

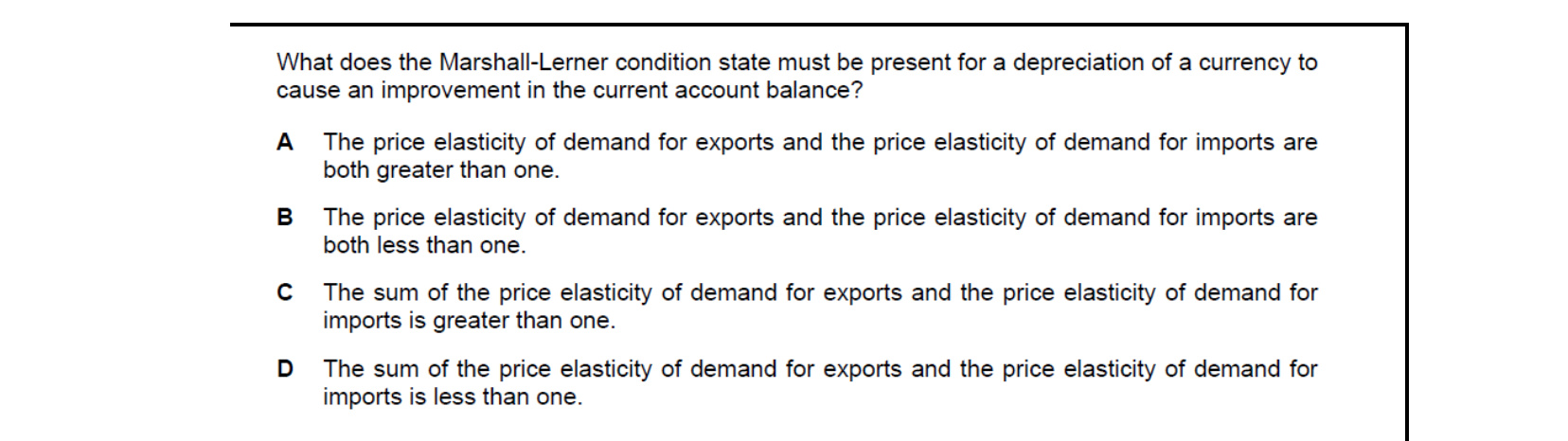

The Marshall-Lerner condition states that a fall in the exchange rate will improve the trade balance only if the combined price elasticities of demand for exports and imports are greater than 1. When this condition is satisfied, a depreciation reduces a current account deficit, and an appreciation reduces a current account surplus.

The intuition is that a depreciation lowers the foreign-currency price of exports and raises the domestic-currency price of imports. The current account improves only if the resulting quantity responses are large enough - more exports sold and fewer imports bought - to outweigh the price effects. The greater the combined elasticities, the smaller the depreciation needed to improve the position. If the sum is less than 1, depreciation will worsen the trade balance, and a revaluation would be the more appropriate strategy.

The J-curve effect

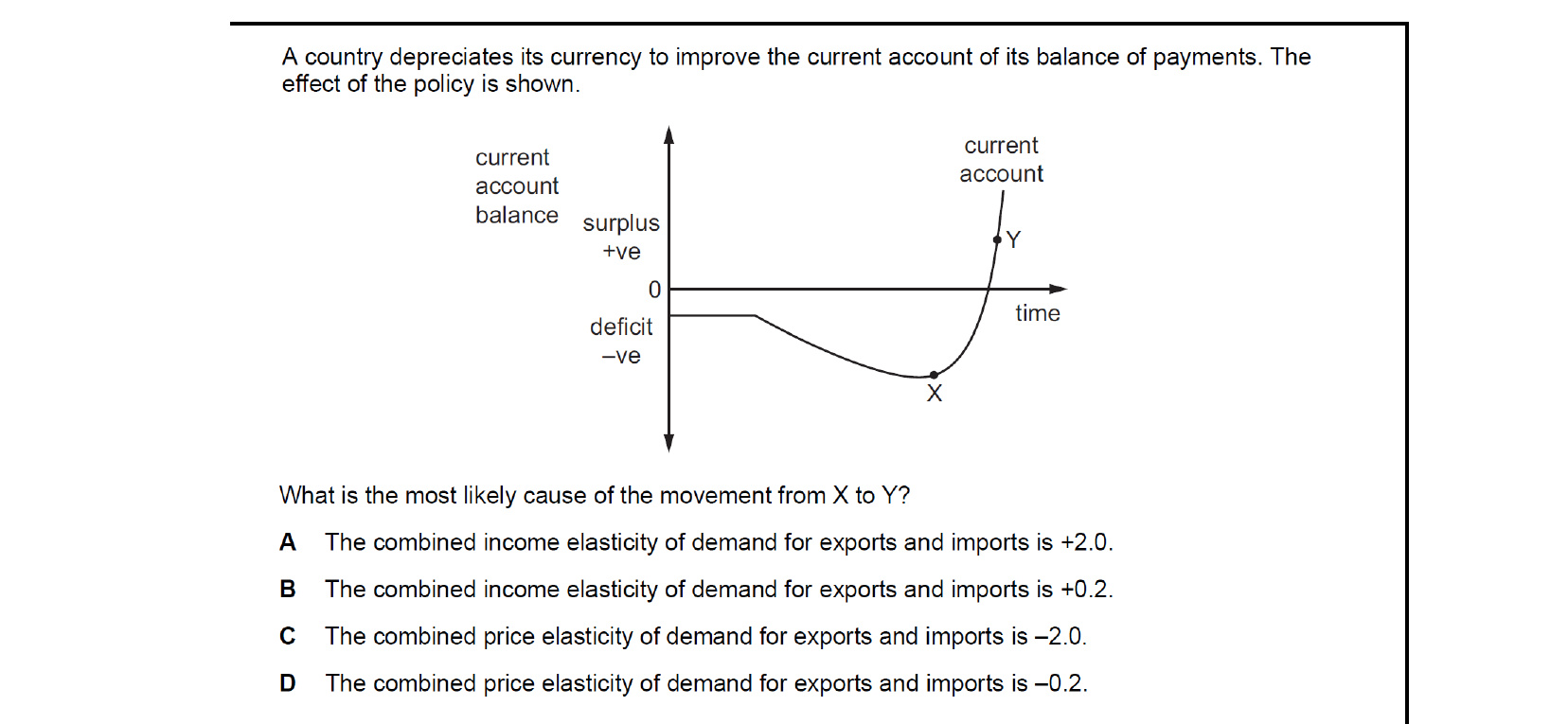

The J curve effect (see Figure 49.9) is closely related. In the short run, demand for exports and imports is often relatively inelastic - buyers take time to recognise that prices have changed and to search for alternative products. A depreciation can therefore make a current account deficit worse before it improves it: the price effects (more expensive imports, cheaper exports in foreign currency) hit immediately while the quantity effects (more exports sold, fewer imports bought) accrue later. Plotted against time, the path of the current account balance traces out the shape of the letter J - first dipping further into deficit, then turning upward and improving as elasticities rise in the longer run.

The same logic operates in reverse for a revaluation. A higher exchange rate may initially widen a current account surplus before reducing it, provided the Marshall-Lerner condition holds in the long run. This is the reverse J-curve (see Figure 49.10).

Key concept link - Time

Differences in the short run and longer run response to a change in the exchange rate are the reason for the J curve effect.

An appreciation makes imports cheaper in the home currency — so imported inflation falls. With Marshall–Lerner holding, the same appreciation also worsens the current account (exports dearer, imports cheaper, demand switches abroad). Weaker net exports reduce aggregate demand and the derived demand for labour, so unemployment rises. Hence imported inflation falls while unemployment rises.

Marshall–Lerner states that a depreciation improves the current account only when the price-elasticity of demand for exports plus the price-elasticity of demand for imports together exceed one. Each elasticity alone need not be greater than one — it is their sum that must clear the threshold so that the quantity gains outweigh the higher import bill.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

A reverse J-curve after a revaluation means the surplus initially widens before declining. The current account surplus increases in the short run as price effects dominate, then narrows in the long run as quantity effects respond. (Note: based on the question shown about depreciation, the Marshall-Lerner-style answer C with combined PED = −2.0 satisfies |PEDx + PEDm| > 1, so the depreciation successfully moves the current account from deficit X to surplus Y.)

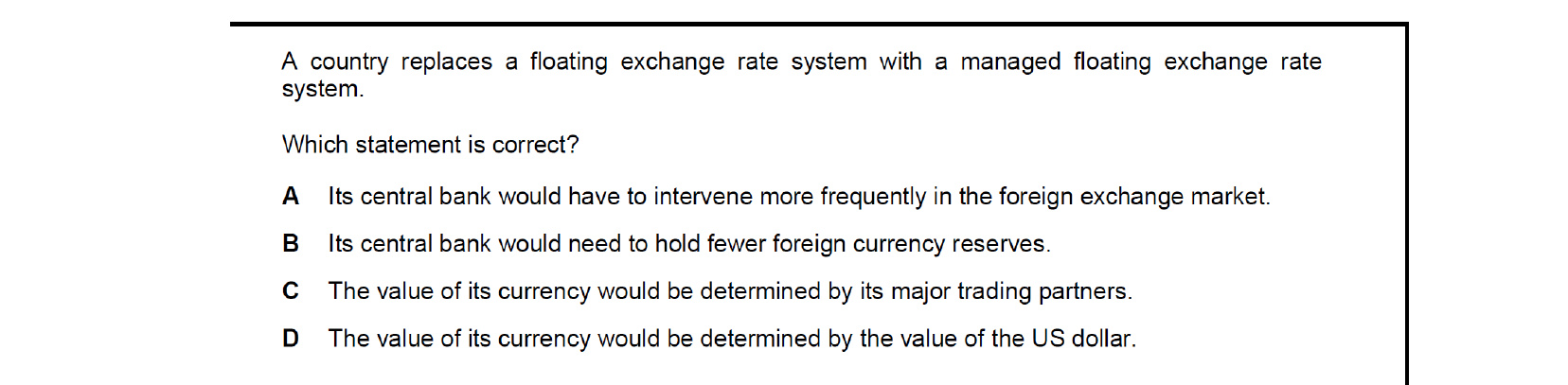

Moving from a free float to a managed float means the central bank now sets a target band or actively leans against undesired movements. To do this it must enter the foreign-exchange market more often, buying or selling the home currency. So the correct statement is that its central bank would have to intervene more frequently in the foreign exchange market.

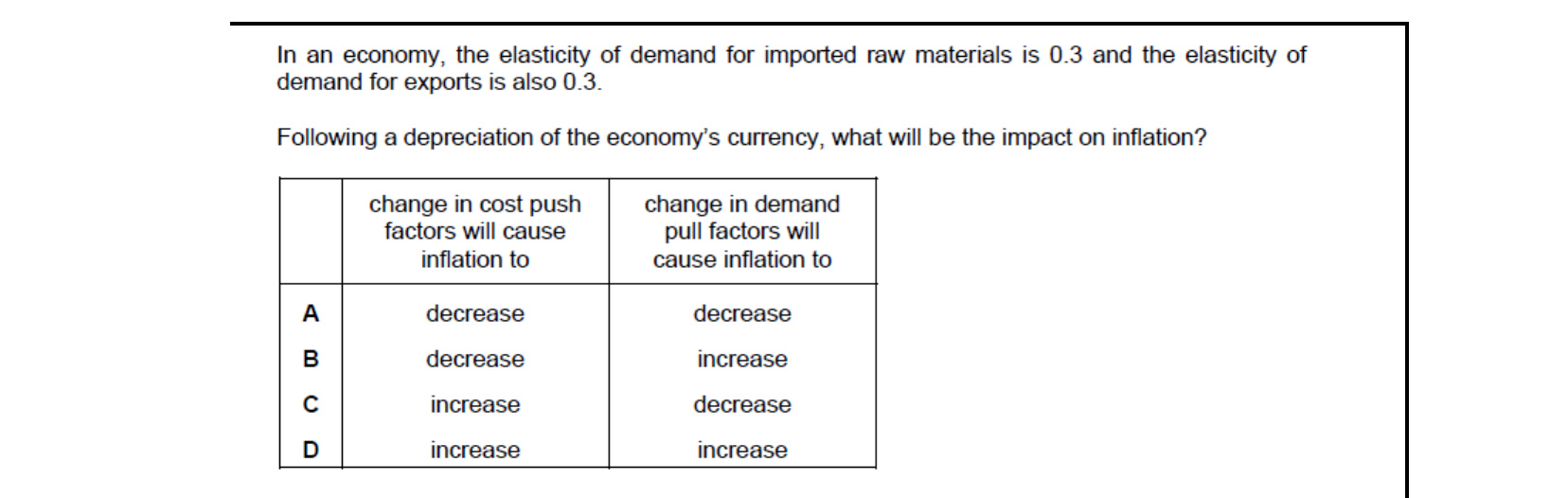

After a depreciation, the home-currency price of imported raw materials rises immediately — and because PED for those imports is only 0.3, firms keep buying nearly the same quantity. Costs rise, pushing cost-push inflation up. Exports become cheaper abroad and (with low export PED) earn more domestic revenue, raising AD and demand-pull inflation. Both forces push inflation up.

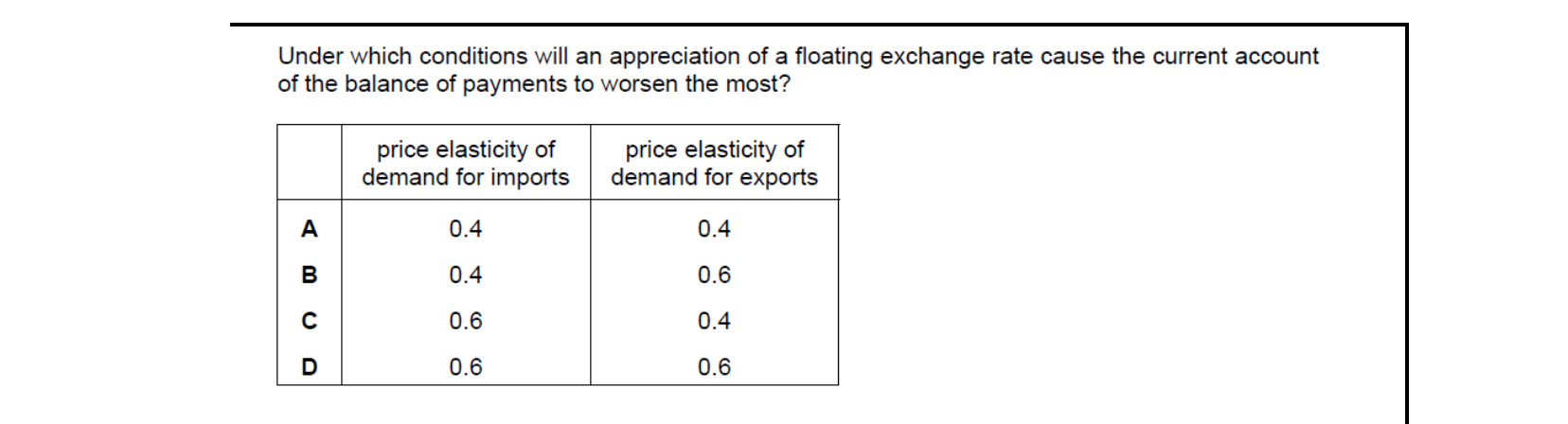

Marshall–Lerner says the current account worsens most after an appreciation when the sum of the PEDs for imports and exports is largest (well above 1) — buyers switch most readily away from now-dearer exports and towards now-cheaper imports. Among the options, both elasticities at 0.6 give the largest sum (1.2), producing the biggest worsening of the current account.

Marshall–Lerner states that, for a depreciation to improve the current account, the sum of the price elasticity of demand for exports and the price elasticity of demand for imports must be greater than one. Each elasticity alone need not exceed one; what matters is that the combined responsiveness is large enough so that quantity effects outweigh the worse import-price effect.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Explain the methods used to measure the price of a currency: nominal foreign exchange rate, real exchange rate, trade-weighted exchange rate.

- Analyse how exchange rates are determined in a fixed rate exchange rate system and a managed system.

- Explain the difference between revaluation (a rise in the fixed exchange rate) and devaluation (a fall in the fixed exchange rate).

- Analyse the causes of changes in the exchange rate under a fixed exchange rate system and a floating exchange rate system.

- Evaluate the effects of changing exchange rates on the external economy using the Marshall-Lerner condition and J-curve analysis.

Want more practice? Drill this chapter's past-paper MCQs (84 questions) →